After several years of development-led growth, the sector is now beginning to attract serious attention from a wider range of capital sources, signalling the early stages of institutionalisation.

While institutional investment has not yet fully entered the market at scale, the structures, pipeline and investor mandates now emerging suggest that this is beginning to change.

A Broader Pool of Capital is Assessing the Sector

Investment processes for co-living opportunities are now attracting a variety of capital sources, including core+, value-add, private equity and family office funds. This diversity reflects the stage of maturity the sector is currently in, with investors approaching opportunities from different risk and return profiles.

However, most transactions completed to date have not followed the traditional institutional acquisition model. Instead, they have largely been structured through funding structures, joint ventures or direct development deals — capital partnering directly with developers and operators to achieve the return thresholds required for the development and operational risk involved.

Institutional Capital Has Yet to Be Fully Tested

The most recent generation of co-living schemes that are now operational or approaching stabilisation have largely not yet been brought to the open market. As a result, the appetite of institutional investors has not yet been tested or proven at scale.

Early Forward Funding Discussions Emerging in Central London

There are a small number of prime central London co-living schemes being marketed quietly via a funding structure. These opportunities are progressing through gateway approvals, and the eventual outcomes and deal structures will provide an important indicator of how institutional capital begins to enter the sector.

Limited Forward Funding Across Residential Has Slowed Entry

We have not seen UK core pension fund capital entering the co-living market from a forward funding perspective. However, this is not unique to co-living.

Across the wider residential sector, the volume of forward funded development deals has been limited due to viability challenges and market conditions. As a result, the absence of core institutional capital in co-living should be viewed in the context of broader market dynamics rather than a lack of interest in the asset class itself.

Planning Constraints Are Restricting the Delivery Pipeline

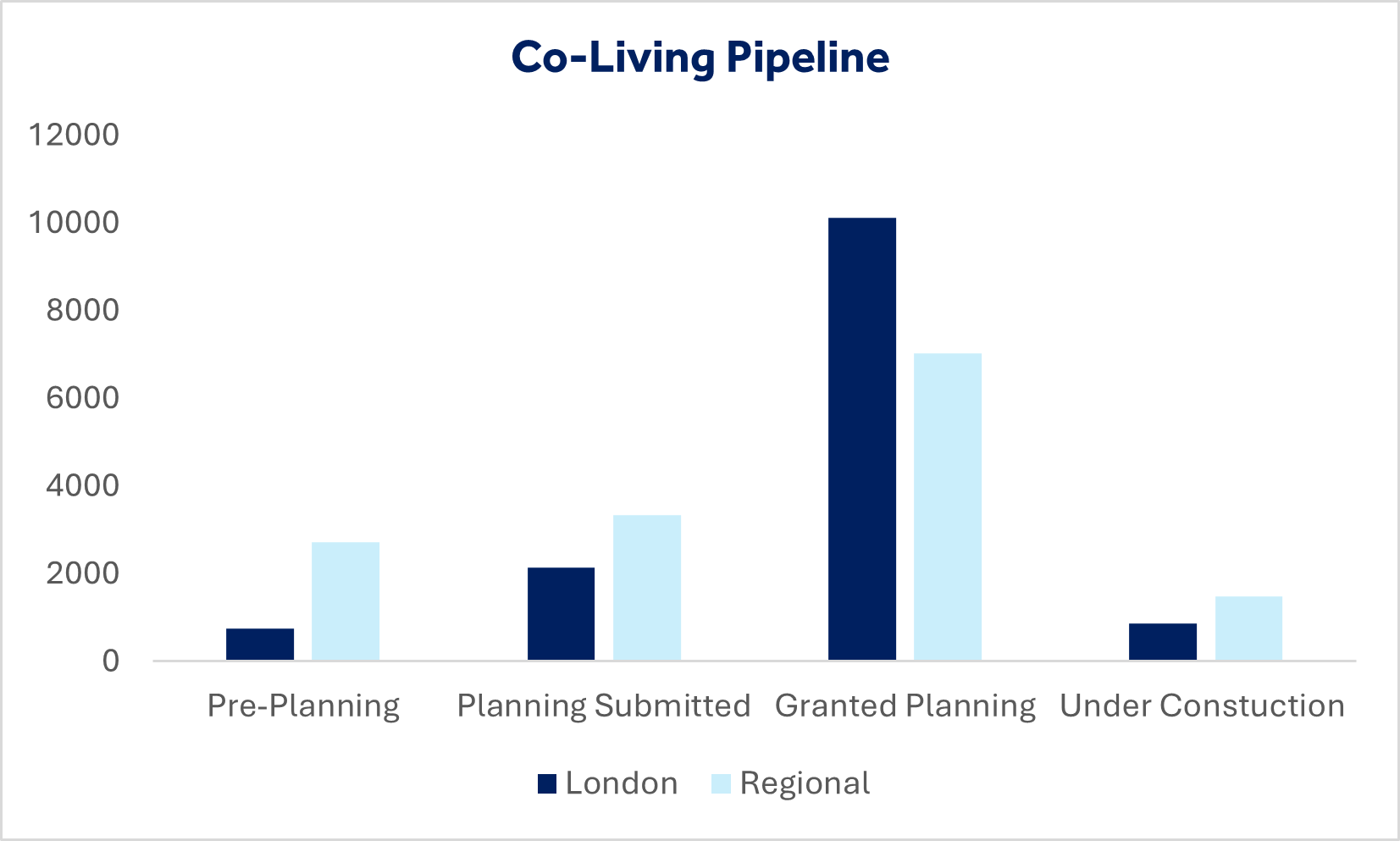

Despite ongoing challenges around gateway approvals and development viability, the co-living sector has built a significant pipeline. The headline numbers are striking:

- Around 8,900 units are currently progressing through the planning process

- A further 17,000 units have already secured planning permission

- However, only around 2,300 units are currently under construction

- Over 12,000 co-living homes in London remain stuck within the planning system, either pre-consent or awaiting further approvals

This highlights that the majority of schemes are struggling to transition to breaking ground, limiting the ability for developers to deliver new homes across the UK and meet the government's housebuilding plans.

The chart above illustrates the number of co-living homes at each stage of planning. (Bidwells)

This data is drawn from Bidwells' proprietary BTR Database, which tracks live information on every BTR development operational and at pipeline stage nationwide.

A Shift Expected Over the Next 12–24 Months

This dynamic is expected to evolve. As more schemes move through the planning system and obtain the necessary approvals, the volume of deliverable co-living opportunities should increase.

If this coincides with improved financing conditions, lower interest rates and stabilising yields, the market is likely to see greater institutional participation in the sector.

Capital Positioning Ahead of the Market

To date, co-living schemes brought to market have largely been offered on a forward commitment basis, reflecting the funding requirements of developers at this stage of the cycle.

In response, a number of fund mandates have been established specifically to acquire sites from developers and deliver co-living schemes directly. By taking on development risk, these investors are seeking to capture the full development and operational value creation available within the sector.

Ready to Navigate the Co-living Opportunity?

The co-living sector's institutionalisation represents both significant opportunity and complexity. Whether you are an investor assessing entry points, a developer seeking capital, or a landowner considering options, our Operational Living team can help you understand the implications specific to your situation. Get in touch with them here.

Image credit: Adam Firman