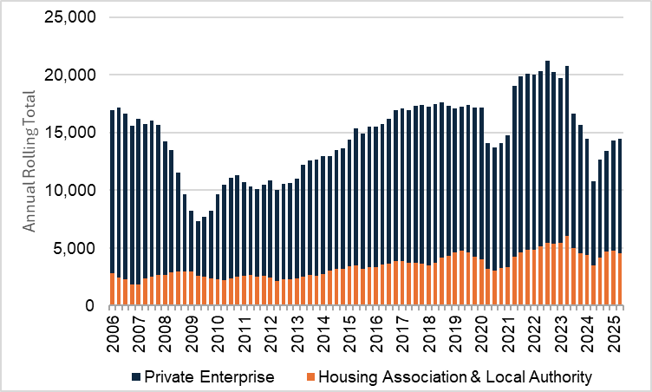

2025 saw a modest recovery in housebuilding in the Ox-Cam Corridor, with starts up 17% in the first half of the year compared with 2024. While this marks progress, activity remains well below the 2022 peak, before interest rates began to rise. Starts are also around 40% below the government’s target of 26,000 homes per year, highlighting the scale of the Corridor’s housing shortage.

Housing Starts in the Ox-Cam Corridor

Source: Bidwells, ONS. 2025

Despite recent reforms, the planning system remains a barrier, particularly for small and medium-sized housebuilders. As many costs are fixed, the planning cost per plot for schemes of fewer than 50 homes has the potential in certain circumstances to now be more than double that of larger developments.

The government has signalled a more decisive overhaul of the National Planning Policy Framework (NPPF), with proposals to introduce clearer, more rules-based national policies. Measures include a permanent presumption in favour of sustainable development, stronger support for development on suitable urban land, and a “default yes” for appropriate sites around rail stations in major economic centres — all particularly relevant to the Ox-Cam Corridor.

Targeted reforms have also been announced to support small and medium-sized housebuilders, including simpler and more proportionate information requirements, greater allocation of smaller sites in Local Plans, and potential exemptions from the Building Safety Levy and BNG for smaller schemes. These changes could help address some of the structural barriers highlighted in our analysis of the unintended consequences of the NPPF. However, as explored in Home truths: builders won’t build if they can’t sell, planning reform alone will not be enough to unlock delivery.

Supply is further constrained by the reduced capacity of housing associations to enter into new Section 106 agreements. Registered Providers are increasingly focused on maintaining existing stock to meet new environmental and safety standards, leaving some mixed-tenure schemes on pause despite planning permission being in place.

The most immediate concern for housebuilders is demand. Buyer confidence in 2025 was affected by economic uncertainty and affordability pressures. Although the government has pledged not to raise income tax, National Insurance or VAT, measures announced in the Autumn Budget mean the average household is expected to be worse off by 2029.

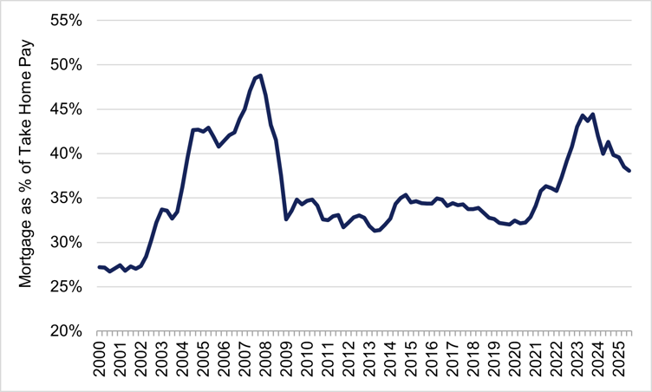

Affordability remains a major barrier. Mortgage payments account for 38% of take-home pay for first-time buyers in the Outer South East, above both the long-term average of 34% and the 30% affordability threshold. Although this has eased as mortgage rates have fallen, rising private rents continue to make it harder for buyers to save for deposits.

First-Time Buyer Affordability

Source: Nationwide. 2025. Note: data are for the Outer South East.

In summary, housebuilders are likely to remain cautious until there are clearer signs of a sustained recovery in demand. Financial markets expect further base interest rate cuts, but these alone are unlikely to be sufficient. Additional targeted support for first-time buyers would help unlock demand and stimulate delivery.

There are, however, some grounds for cautious optimism. The Budget confirmed a permanent 95% mortgage guarantee scheme and measures to strengthen planning capacity. Combined with expected interest rate cuts, these steps could help support Halifax’s forecast of modest house price growth of 1%–3% in 2026 and point to stronger housing delivery.